Compensation is one of the most important tools for motivating and retaining field salespeople. However, designing compensation plans tends to be a derivative rather than a lead process. For example, a paper distributor faces a mature market with average gross margins of 18 to 20 percent. Salespeople are paid commissions of 20 percent of gross margin to center their attention on boosting distributor profits. Although this plan looks good, gross profit growth mysteriously results in a decline in net profits. The sales reps would rather focus on small orders they can turn around quickly than spend time working for the big order. However, the small orders have higher processing and delivery costs. Thus, growth in small orders raises overhead faster than the increase in gross profit. The paper distributor needs a plan that will maintain gross profit margins and also reach its goals for net profits. To meet both goals, the distributor must create a plan that links commission rates to gross profit and order size. Instead of one gross margin commission of 20 percent, the distributor needs to vary the size of commissions with the size of the gross margin percentage achieved on each order and on the gross margin dollars earned on each order. The result is a plan that ties reps’ commissions to their true contribution to the company’s profit goals.

This example shows that compensation plans must be custom designed to meet the goals of individual firms. It also shows that the natural desire of salespeople to make money for themselves sometimes conflicts with the firm’s need to control expenses. This means you have the difficult task of designing compensation programs that motivate salespeople to reach company goals without bankrupting the firm at the same time. Since 30 to 40 percent of all sales reps are unhappy with their compensation plans at any one time, you are continuously challenged to come up with a better program.

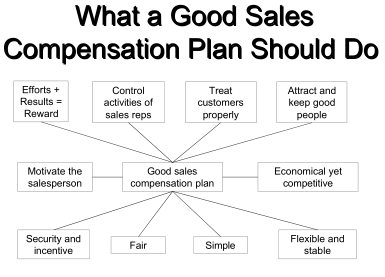

The sales compensation plan is an essential part of the total program for motivating sales personnel. A sales compensation plan, properly designed, has three motivational roles:

- Provide a living wage,

- Adjust pay levels to performance, thereby relating job performance and rewards (in line with expectancy motivation theory), and

- Provide a mechanism for demonstrating the congruency between attaining company goals and individual goals (also in line with expectancy theory).

A properly designed sales compensation plan fits a company’s special needs and problems, and from it follows attractive returns for both the company and its sales personnel. Sales and growth goals are reached at low cost, and profits are satisfactory. Sales personnel receive high pay as a reward for effective job performance, and esprit de corps is high.

In established companies it is rarely necessary to design new sales compensation plans, and sales executives concern themselves mainly with revising plans already in effect. Most changes are minor, instituted to bring the plan and marketing objectives into closer alignment. If, for example, additional sales effort is needed for the factory to operate at optimum capacity, an adjustment in compensation may be required. This could mean paying bonuses on sales over the quota, paying additional compensation for larger orders or for securing new accounts, or revising commission rate schedules. Any change, of course, could be either temporary or permanent.

There are two situations where total overhauling of compensation plans are in order.

One is the company whose sales force already has low morale, perhaps because of the current compensation plan. If the plan is at the root of the morale problem, drastic change is appropriate. A second situation calling for a complete revamping of the sales compensation plan occurs when a company is anticipating the cultivation of new and different markets.

The problems in these two situations are like those in the newly organized company, which must build its sales compensation plan from scratching both cases management_ must consider many factors, the nature and number of which vary with the company and the situation, but usually include the types of customers, the marketing channels characteristics of the products, intensity of competition, extent of the market and complexity of the selling task.