Let’s learn about journal. Business transactions involve the exchange of value either in form of money or of goods or services measured in terms of money. Book-keeping has been defined as “the art of recording business transactions” with a view to recording transactions permanently and thereby showing their effect on wealth. It is a science that records transactions in such a manner that a trader is able to ascertain the nature and value of assets, the number of liabilities including the amount he owes to the creditors, profit, and loss during a given period, etc.

Definition of Journal

Journal is a primary book of accounts in which transactions are originally recorded in a chronological (day-to¬day) order. It is called the book of original entry. Journal records all transactions, these transactions are either written, as they occur, in a rough book or on the various documents. On the basis of the entries made in the documents the accounts are to be debited and credited carefully in a systematic manner. All the transactions are recorded in a book which is known as the journal.

Examination of Dual-effect of Accounting

Since every transaction have a dual effect, therefore the resulting Accounting Equation obtained states that at any point of time money value of assets of an entity must be equal to the total of owner’s equity and outsider’s liabilities. This may be expressed in the form of an equation:

Assets – Liabilities = Capital (Owner’s Equity)

In case of complex or compound transactions, all the fundamental elements may be affected simultaneously in a number of ways. The Accounting Equation gives:

Liabilities + Capital = Assets

Journal book records all transactions, these transactions are either written, as they occur, in a rough book or on the various documents. On the basis of the entries made in the documents the accounts are to be debited and credited carefully in a systematic manner. All the transactions are recorded in a book which is known as the journal. This can be illustrated from the below example

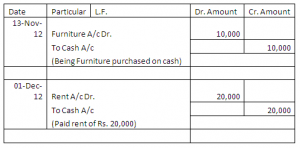

-

- Nov 13, 2012: Purchase furniture for cash of Rs. 10,000

- Dec 1, 2012: Rent paid Rs. 20,000

The following entry will be recorded in the journal book as follows:

Each entry in Journal normally contains the following six parts:

(i)Date

(ii) Title of accounts to be debited

(iii)Debit amounts

(iv)Titles of accounts to be credited

(v)Credit amounts

(vi) Explanation